In this section of the report, we include some topline data about digital progress across the UK, with specific sections dedicated to Wales and Scotland. The data for all responses for these groups are available on our website for further investigation.

Regional differences in digital maturity

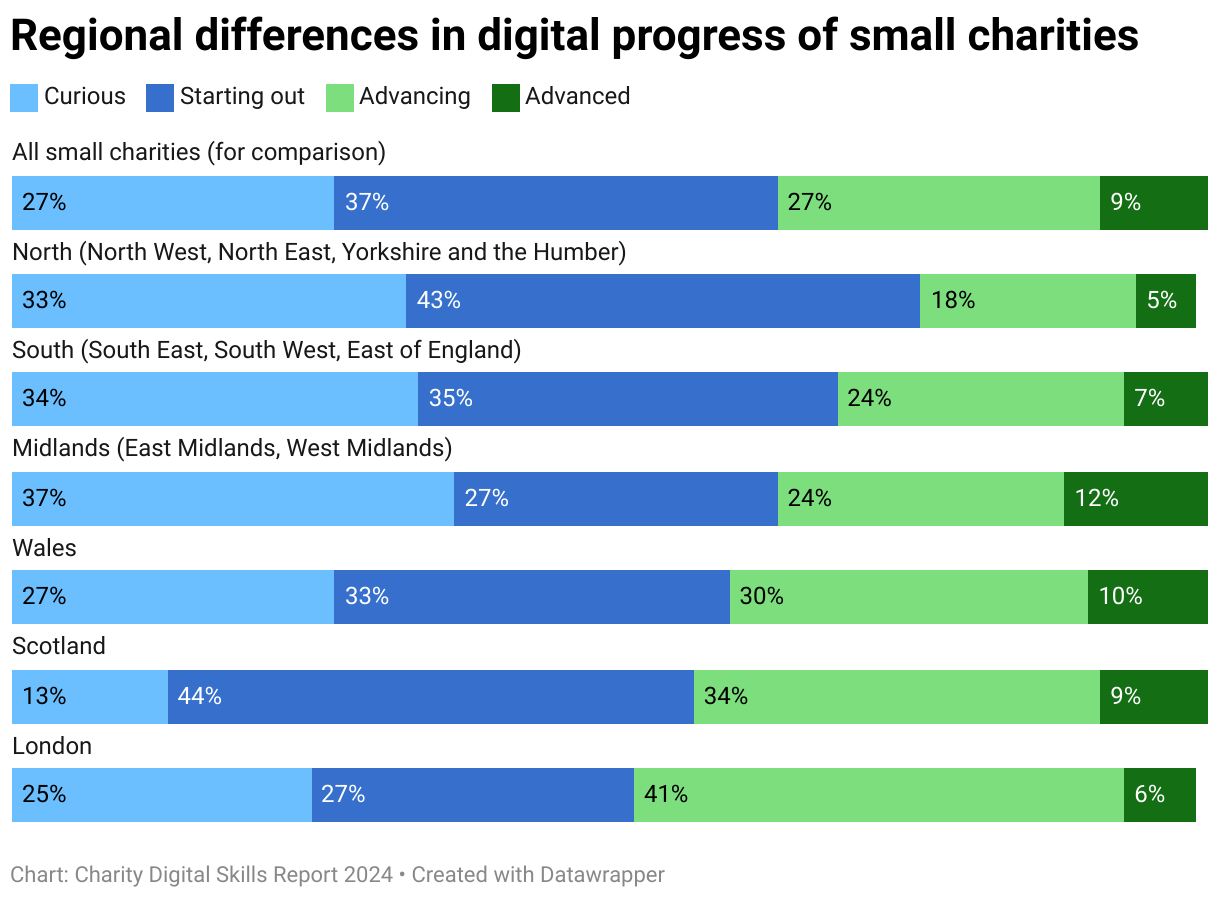

Throughout this report, you will see that size plays a crucial role in digital capacity and the responses given. Overall, larger charities are much further ahead with digital. In our sample, the proportion of large and small charities varies significantly in each region or country (a breakdown can be found in ‘UK nations and regions in our sample’). For this reason, we have compared the digital stages of small charities across each region.

Overall, we can see that there are higher proportions of small charities at the earliest stages with digital in the North of England (combining the North West, North East and Yorkshire and Humber) and South of England (excluding London, including the East of England, South East and South West), compared to the rest of the UK.

- North of England (North West, North East and Yorkshire and Humber): 76% of small charities are at an early stage with digital, higher than the 64% of all small charities. A third of small charities in the North East are at the curious stage of digital (33%).

- South of England (East of England, South East and South West): 69% of small charities are at an early stage with digital, slightly higher than the 64% of all small charities. A third of small charities in the South are at the curious stage (34%).

- Midlands (combining East Midlands and West Midlands): Has the highest proportion of charities (37%) saying they are at the earliest curious stage of digital. Overall, 64% of small charities are at an early stage with digital, in line with the rest of the UK.

- London: Half (52%) of small charities are at an early stage with digital, which is lower than the 64% of all small charities across the UK. A quarter (25%) of small charities in London are at the earliest, curious stage with digital.

- Wales: Note, this has a small sample size of 30 small charities in Wales, which may affect the results. In this group, 60% are at an early stage with digital.

- Scotland: Note, this has a small sample size of 32 small charities in Scotland, which may affect the results. In this group, 57% are at an early stage with digital.

Wales

Whilst charities in Wales look to be further ahead with digital in comparison to our main sample, this is influenced by the high proportion of large charities. Capacity and headspace for organisational development is a key challenge in Wales, with 73% saying this is what they most need funding for (compared to 57% of all charities and 59% of large charities). Offering or improving digital services, as well as investing in infrastructure and systems, are also key priorities for charities in Wales.

Our sample

- 62 of our responses (10%) are based in Wales. 87% are a registered charity or Charitable Incorporated Organisation (CIO), 8% are a company limited by guarantee.

- 48% are small, 48% are large (the remainder did not specify). This is a greater proportion of large charities compared to the 32% in our main sample.

- 16% describe themselves as a social enterprise or community business.

- 6% are infrastructure or second tier organisations.

- 34% are led by people with lived experience of the issue they address.

- 65% are providing frontline services to individuals, compared to 53% in our main sample.

Digital progress

- 44% are at an early stage with digital (16% curious and 27% starting out), whilst 56% are advancing or advanced, with a strategy in place for digital. This is similar to 2023 and is influenced by the high proportion of large charities responding in Wales.

Barriers to digital progress

- A lack of headspace and capacity (74%)

- Squeezed organisational finances (72%)

- Finding funds to invest in infrastructure, systems and tools (60%)

Digital priorities

- 84% see digital as an organisational priority, with 21% saying it is a high priority.

- 33% say their top priority this year is to develop a digital strategy, whilst 39% say their top priority this year is to develop a data strategy.

- Top priorities are similar to our overall sample for large charities. These are:

- Use data to improve services or operations (58%)

- Increase online fundraising (56%)

- Grow our reach (56%)

- 46% plan to invest in their infrastructure and systems this year.

Services

- 79% are delivering services built on digital tools, in a supportive or integral role.

- 61% are using digital tools behind the scenes to help run services.

- 11% support clients with digital inclusion, whilst 21% say this is a priority.

- 63% feel their services are inclusive to some extent (41%) or a great extent (21%).

- In the next year, 26% say their priority is to develop or scale digital services, whilst 28% plan to offer new digital services. This is greater than the 18% of all respondents.

AI

- 62% are currently using AI in their day-to-day work or operations.

- 46% say that using AI tools is a priority this year.

- 24% are using AI tools behind the scenes to deliver services.

- 71% agree or strongly agree that AI developments are relevant to them, whilst only 25% feel prepared to respond to AI opportunities and challenges.

Funding

- 25% accessed funding for some digital costs, such as new devices or staff time.

- 6% accessed funding for substantial digital costs (such as a digital role or website).

- The top barriers to accessing digital funding are:

- We need to prioritise paying the bills and other core costs (41%)

- We prioritise meeting demand and delivering our current work (39%)

- Our typical funders do not cover digital costs (31%)

- Our typical funders do not cover staff costs/time on digital/data (24%).

Top funding needs

- Capacity/headspace for organisational development (73%).

- Someone internally to lead on digital change (50%).

- Development of existing digital services and products (40%).

- Bring in external advice/expertise (40%).

Scotland

Whilst charities in Scotland look to be further ahead with digital in comparison to our main sample, this is influenced by the high proportion of large charities. Capacity and headspace for organisational development is a key challenge in Scotland. Equipment, hardware and devices (e.g. laptops) as well as limited access to the internet and wi-fi connectivity are slightly bigger challenges in Scotland, compared to other countries and regions.

Our sample

- 64 organisations (10% of our responses) are based in Scotland.

- 51% are small, whilst 40% are large (the remainder did not specify). This is much greater than the 32% of large charities in our main sample.

- 79% are a registered charity or Charitable Incorporated Organisation (CIO), 19% are a company limited by guarantee.

- 16% describe themselves as a social enterprise or community business.

- 8% are infrastructure or second tier organisations.

- 22% are led by people with lived experience of the issue they address, compared to 31% of our main sample.

- 60% provide frontline services to individuals, compared to 53% in our main sample.

Digital progress

- 41% are at an early stage with digital (8% curious and 33% starting out), compared to 50% of all charities. This is similar to 2023 and is influenced by the high proportion of large charities responding in Scotland.

- 59% are advancing or advanced, with a strategy in place for digital.

- 30% say they are struggling because of their equipment, hardware and devices (e.g. laptops) (30%). This is much higher than the 18% of our main sample.

Barriers to digital progress

- Squeezed organisational finances (72%).

- Finding funds to invest in infrastructure, systems and tools (67%).

- Lack of headspace and capacity (65%).

- Equipment, hardware and devices (e.g. laptops) are an issue for 30% of charities in Scotland. This is affecting a greater proportion of charities, compared to 18% (15% of large and 20% of small charities) of the main sample.

- Limited access to the internet and wi-fi connectivity is affecting 13% of charities, compared to 5% in the main sample, indicating this is a bigger challenge in Scotland.

Digital priorities

- 92% see digital as an organisational priority, with 31% saying it is a high priority.

- 35% say their top priority this year is to develop a digital strategy, whilst 44% say their top priority this year is to develop a data strategy.

- Top priorities are:

- Build our online presence and social media engagement (58%)

- Increase online fundraising (54%)

- Use data to improve services or operations (53%)

- Grow our reach (53%).

Services

- 81% are delivering services built on digital tools, in a supportive or integral role.

- 66% are using digital tools behind the scenes to help run services.

- 16% support clients with digital inclusion, whilst 7% say this is a priority this year.

- 65% feel their services are inclusive to some extent (37%) or a great extent (28%).

- In the next year, 25% say their priority is to develop or scale digital services, whilst 30% plan to offer new digital services. This is greater than the 18% of all respondents.

AI

- 61% are currently using AI in their day-to-day work or operations.

- 15% are using AI tools behind the scenes to deliver services.

- 70% agree or strongly agree that AI developments are relevant to them.

- 23% agree or strongly agree that they feel prepared to respond to AI opportunities and challenges.

Funding

- 22% accessed funding for some digital costs (e.g. devices or staff time), whilst 9% accessed funding for substantial digital costs (e.g. a digital role or new website).

- The top barriers to accessing funding are:

- We need to prioritise paying the bills and other core costs (44%)

- We prioritise meeting demand and delivering our current work (41%)

- Our typical funders do not cover digital costs (33%).

Top funding needs

- Capacity/headspace for organisational development (55%).

- Training for staff and volunteers on digital or data (44%).

- Subscriptions/licence costs (36%).

- Develop our digital strategy (35%).